Australians’ love of the bricks and mortar shopping experience, and the convenience of Australia’s large shopping centre network, has played a key role in slowing the growth of ecommerce relative to other countries. However, it has been a constant battle, according to a new report by KPMG, Beyond COVID-19 – the shifting foundations in retail property.

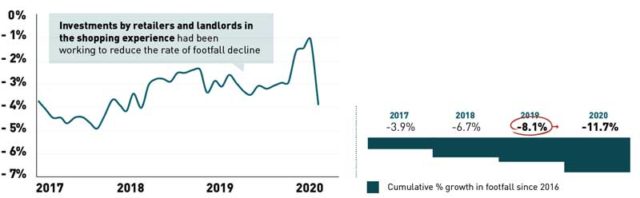

Retail precinct footfall had been in decline for years as e-commerce penetration gradually grew – recording 8.1 percent in cumulative footfall losses over the 3 years to 2020. Retailer profit margins and retail landlord yields were being squeezed, and consumer confidence had been in decline for most of 2019 following a turbulent year of Royal Commissions, rising public concern regarding the cost of living and house prices, stagnant wage growth, prolonged drought, the Black Summer bushfires, and other severe weather events.

Retail precinct footfall had been in decline for years as e-commerce penetration gradually grew – recording 8.1 percent in cumulative footfall losses over the 3 years to 2020. Retailer profit margins and retail landlord yields were being squeezed, and consumer confidence had been in decline for most of 2019 following a turbulent year of Royal Commissions, rising public concern regarding the cost of living and house prices, stagnant wage growth, prolonged drought, the Black Summer bushfires, and other severe weather events.

The role of bricks and mortar retail has been transformed overnight by Covid-19. The onset of physical distancing measures swiftly changed consumer behaviour – from how much people buy online, how often they visit physical stores and what days and times they shop, to how far they travel on each shopping journey.

For retailers and landlords, the potential that these changes may be permanent escalates challenges regarding brick and mortar channels, given the high fixed-cost of building, operating and trading through them.

Some of the key findings from the KPMG report are:

Living local has triggered a rebirth of village shopping: Throughout Covid-19, people have rediscovered their local stores and neighbourhood shopping precincts. They have likely established stronger connections with their local business community and saved valuable travel time. Some of this change may be permanent given the extended duration of behavioural change, and the value of smaller shopping precincts could grow and become more competitive. Given the overall expectation of reduced demand for physical retail space, this growth would come from other precincts such as CBDs or large shopping centres.

A new rhythm for the ‘weekly shop’ is emerging: Sunday and Monday have become the favoured 2-day shopping window across most retail precincts, with the exception of the CBD. Almost half of all weekly visits are now occurring on these days, compared to a quarter of visits prior to Covid-19.

Consumers have also changed the time of day that they shop. People are heading to stores earlier in the day – either soon after opening or at lunchtime, instead of picking up supplies on the way home from work after 6pm. Morning and early afternoon shopping trips appear to be a luxury of remote working.

Great safety experiences equal great customer experiences: Customers will seek out retail experiences that are either ‘really safe’ or ‘really snappy’(fast). During Covid-19, when customers share stories about their shopping experiences, they are likely to focus on how safe they felt and how easy it was to get everything they needed quickly. Retailers and landlords need to consider how to adapt their strategies to shift the focus from driving increased dwell times to driving greater spend velocity and consumer advocacy of the safety experience.

Tenants and landlords face a classic ‘prisoner’s dilemma’: Resolving the retail property issue is about trust – a challenge for an industry well known for being adversarial at times. The Covid-19 context creates a unique opportunity for retailers and landlords to find more collaborative and innovative ways to transform the industry without unnecessary duress. Both sides are under significant pressure and both have options to partially release pressure but neither has a perfect hedge. As the ‘prisoner’s dilemma’ shows, achieving a ‘win-win’ outcome will require ‘give and take’ on both sides.

Be prepared and responsive: Amid these challenges, how could Australian retailers and landlords create and share value post Covid-19?

Celebrate being local, and stay close to customers who may have reconnected with your property, store or brand through COVID-19. Continue to invest in your authentic relationship with that community. There is an opportunity to become the safe, trusted destination to experience and enjoy the tactility and physicality of the shopping experience – with transactions happening quickly and seamlessly through technology.

Adjust operations and marketing to the new weekly shopping rhythm where Monday is the new ‘Sunday shop’, and lunchtime is the new ‘after-work shop’ – including workforce planning, re-stocking cycles, security, cleaning, parking management, and marketing and promotion launches.

Differentiate your shopping experience by making it very ‘safe’, or make it ‘snappy’ by enabling faster shopping journeys. For example, offer shopping concierge services, introduce senior citizens’ shopping hours, and offer pre-booked fitting rooms, especially during the upcoming peak trading and Christmas period.

Retailers and landlords need to build trust and work together to consider ways to share the challenges and the opportunities exacerbated by Covid-19 to achieve a win-win outcome and succeed in transitioning their models at the lowest cost. This could involve experimenting with new store and property service models to create mutually beneficial outcomes.

– KPMG

Full Report: Beyond COVID-19 – the shifting foundations in retail property.

Be First to Comment