The CIPA seminar presentation for CP+ 2021 back in January slipped under the radar when CP+ was more or less cancelled went online, but nonetheless contained some market data which is of interest.

The prevailing narrative within an industry which is driven by sales of cameras and lenses is that it is suffering from a chronic, seemingly irreversible wasting disease. But if we take a longer-term view, even after a decade or more of decline, there is still more demand for cameras and lenses today than there was before the ‘digital revolution’ kicked in around the change of the century.

We’ve re-published some of the more interesting charts and graphs from the CIPA seminar below:

TOTAL CAMERA SHIPMENTS IN VOLUME:

The graph makes the point that we are now at about 10 percent of ‘Peak Digital Camera’ and maybe there’s a perception here that we are heading inexorably towards that zero on the Y axis. Expect a big uptick in 2021, if the latest CIPA shipment figures are any indication. As the financial ads fine print says: ‘past performance is no guarantee of future results’. But maybe in a good way in this case.

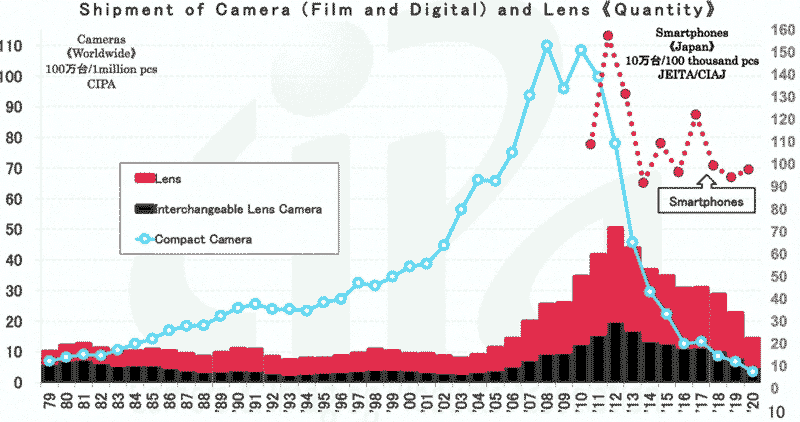

CAMERA & LENS SHIPMENTS 1979 – 2020:

The main take-out from this rather busy graph is that even with the predations of smartphones, there are a shedload more lenses and interchangeable lens cameras being sold now compared to the era prior to digital cameras – say before the year 2000. Compacts – not so much.

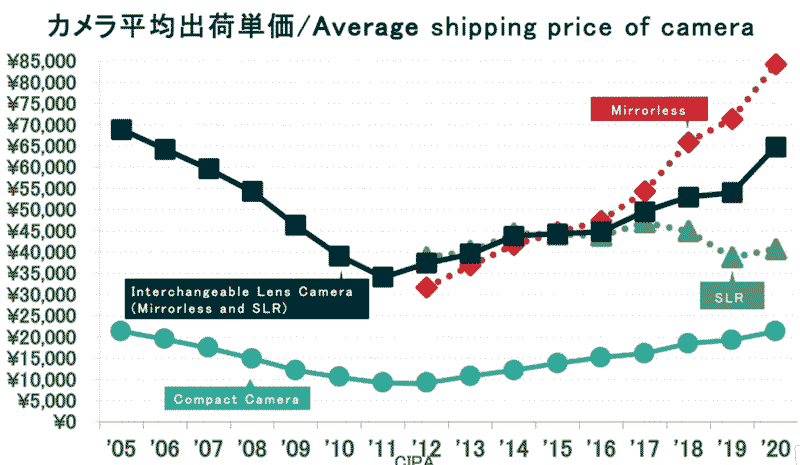

AVERAGE CAMERA PRICES, 2005 – 2020:

While camera sales have been dropping dramatically in volume over the past 10 years, the same can’t be said for average selling prices. This graph clearly illustrates where the money is: DSLRs now represent the budget end of the interchangeable camera market, while mirrorless cameras command a premium. Interesting also to note that compact cameras are increasing in average pricing as the sheer quantity of new models drops off and higher-priced (and higher margin) weatherproof, or ultra-zoom, or premium pocket cameras like the Ricoh GR or Sony RX series own what’s left of the market.

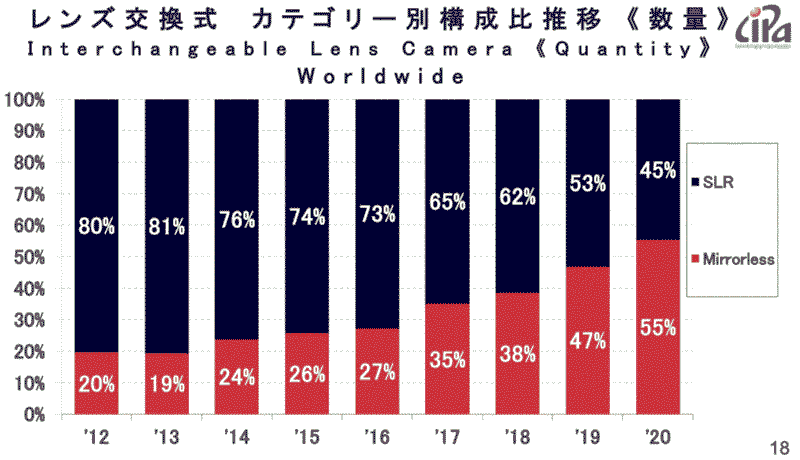

MIRRORLESS Versus DSLR:

2020 will go down in history as the year the WuFlu hit, but it was also the year when mirrorless cameras ended the historical dominance of DSLR technology. The next graph nails it….

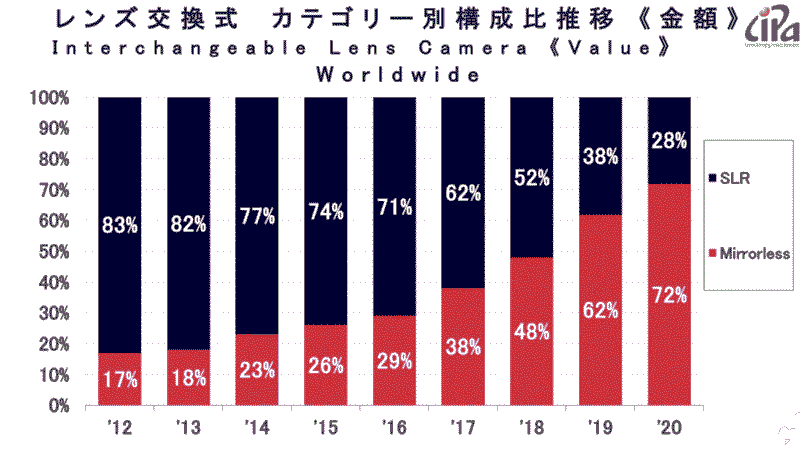

MIRRORLE$$ Versus DSLR:

While DSLR represents 45 percent of the volume in interchangeables, they delivers just 28 percent of the value of the market – around half of what they were doing in 2018.

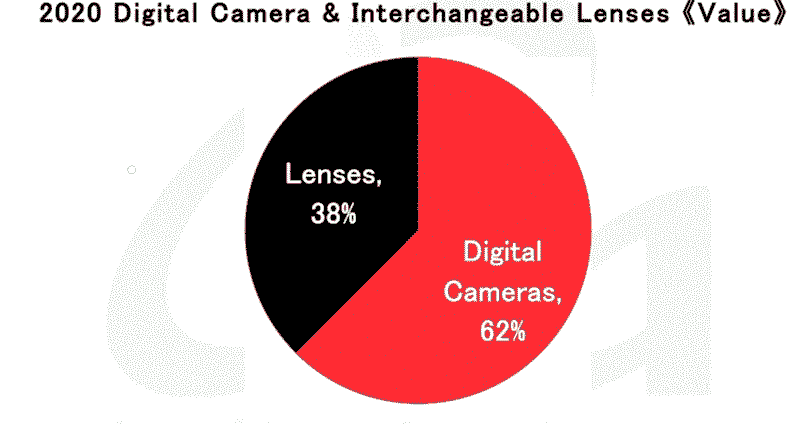

CAMERAS & LENSES – COMPARATIVE VALUE:

Camera stores will probably be aware that lenses represent over one-third of the dollar value of the total market; to most of us it might come as a surprise, given the focus on camera bodies.

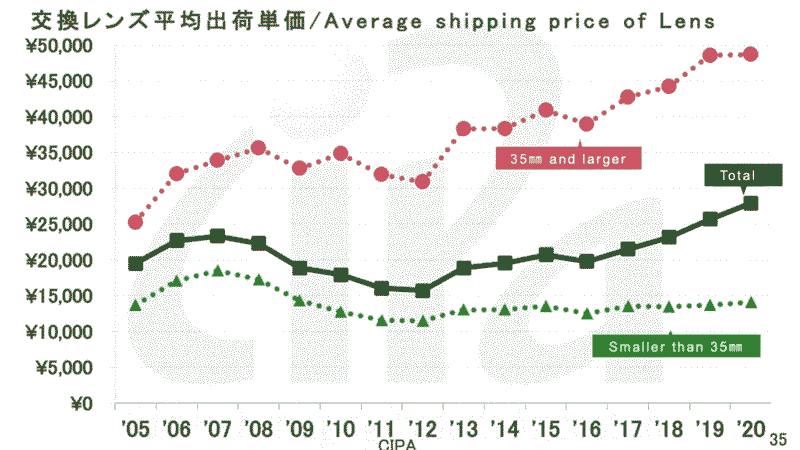

LENS SHIPPING PRICES:

Not surprisingly, lenses for full frame cameras are commanding higher prices, but the huge differential – with unit prices three times higher for full frame than M43 or APS-C format – is more surprising.

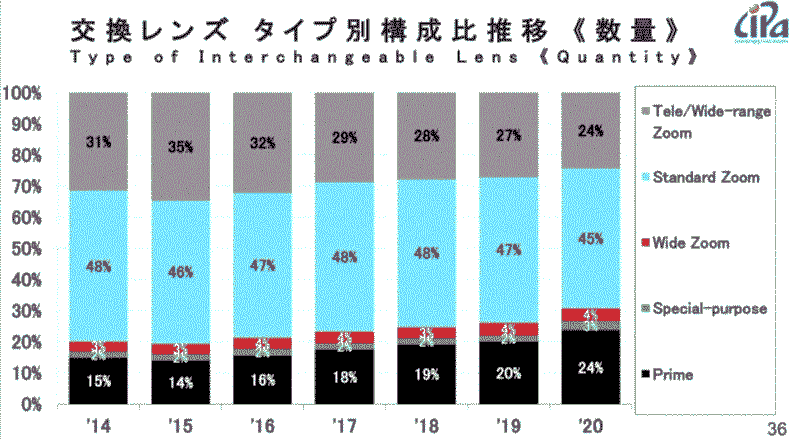

LENS TYPES:

The versatile standard zoom remains the go-to lens, while the growth in demand for prime lenses perhaps indicates increasing sophistication of lens buyers. Or maybe it’s just that all those affordable, high-performance Sigma primes released over the past five years have made them a viable option for enthusiasts!

Be First to Comment